Insurance Learning Center

Does Credit Score Affect Car Insurance Rates?

Does Credit Score Affect Car Insurance Rates? Find out how credit score affects car insurance rates, what insurers look at, and how you can improve your credit-based insurance score to lower your premiums.

Read more

What is a Car Registration Suspension?

What Does Suspension of Registration Mean? Check out our comprehensive guide to learn about the reasons for vehicle registration suspension, its implications, legal consequences, and how to reinstate your registration.

Read more

What is a Proof of Insurance Card and When Do You Need it?

Learn why a proof of insurance card is essential for legal compliance, avoiding fines and filing claims. Auto insurance laws, digital vs paper proof and what happens if you’re caught without one.

Read more

Are Older Cars Cheaper to Insure?

Find out what affects insurance costs for older cars, including depreciation, repair costs and safety features. Get expert advice to help you save. Request a quote today and get the best rates for your car!

Read more

What is a Hardship License or Restricted License?

Trying to Get a Hardship License or Restricted License? Read Everything you need to know. Eligibility, application process, limitations and the differences from regular licenses. For those facing license suspensions or restrictions, looking for legal options to drive to for work, school or for daily essential travel.

Read more

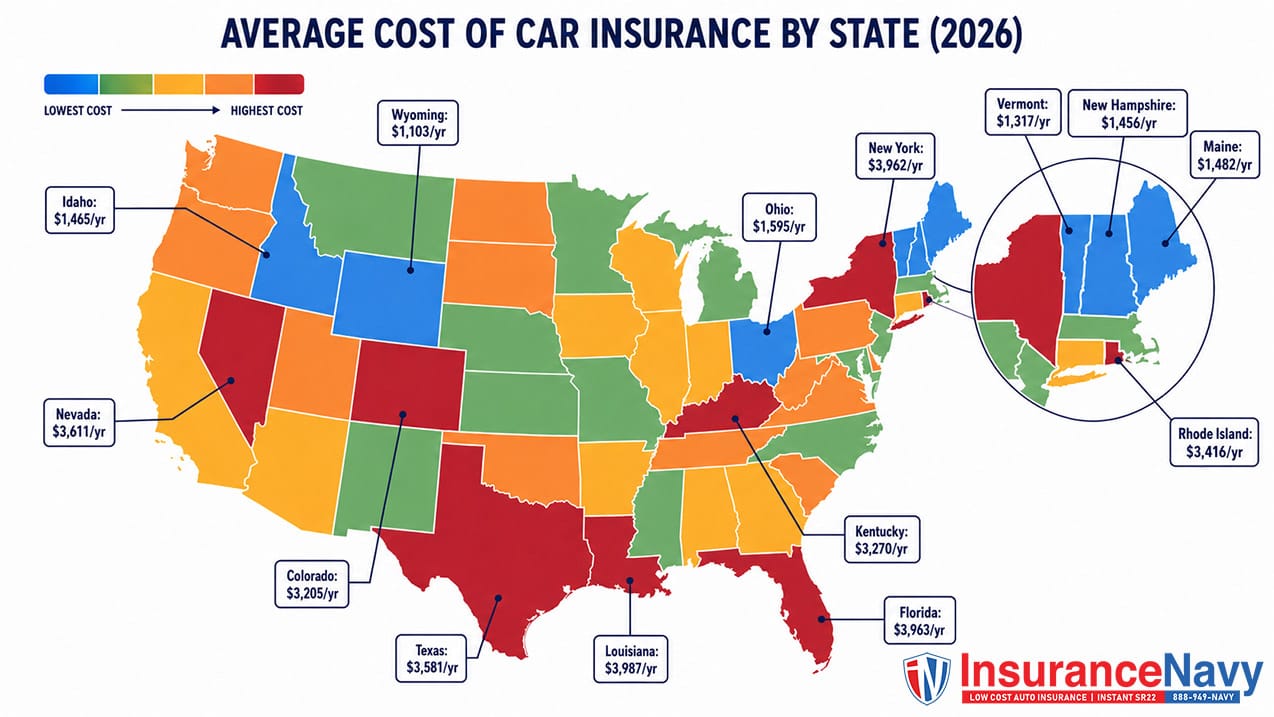

Average Cost of Car Insurance in the USA for 2026

2026 Car Insurance Costs: Find out how location, vehicle type and driving history impact your premiums. Compare rates from top providers and get a quote today to find the best coverage at the lowest price!

Read more

What Happens If You Are At Fault In A Car Accident?

Learn about situations where you’re at-fault in a car accident. Our at-fault accident guide covers legal consequences, insurance claims and tips for dealing with damages and injuries responsibly.

Read more

Does Car Insurance Cover Theft? Stolen Car Coverage Explained

Comprehensive coverage pays your car's actual cash value minus deductible if it's stolen. Liability and collision do not. See what's covered, claim steps, and 2025 NICB theft data.

Read more

The Best Car Insurance Commercials

Watch the most memorable, creative and effective car insurance ads and learn what makes them tick.

Read more

Does Roadside Assistance Count as a Claim?

Find out if roadside assistance counts as a claim and how it affects your insurance premiums. Our comprehensive guide explains how to use roadside assistance and tips to help you make informed decisions about your car insurance.

Read more