Car insurance is a contract that appears as a multi-page policy document and a wallet-sized identification card. A car insurance card lists the insurer name, policy number, coverage dates, and vehicle VIN. The full policy document runs 20 to 50 pages across ten standard sections. Drivers who cannot present proof of insurance during a traffic stop face fines. According to the FHWA, approximately 239.9 million licensed drivers operated in the United States in 2024. Insurance Navy helps drivers find the right insurance at the right price. This guide explains car insurance card fields, declarations pages, policy sections, and digital cards.

Table of contents

- What a Car Insurance Card Looks Like

- Sample Card by Major Carrier

- Digital vs. Physical Cards

- What Your Car Insurance Policy Looks Like

- 1. Declarations Page

- 2. Agreements

- 3. Definitions

- 4. Insuring Agreement

- 5. Conditions

- 6. Types of Coverage

- 7. Coverage Payment Limits

- 8. Deductibles

- 9. Exclusions

- 10. Endorsements and Riders

- Why You Need to Carry Your Car Insurance Card

- Situations Where You'll Need to Show Your Insurance Card

- What Else is on Your Insurance Card?

- Losing Your Proof of Insurance Card

- Embracing Digital Car Insurance Cards

- Ready to Shop for a New Policy?

- Key Takeaways

- Frequently Asked Questions

- What does a car insurance policy actually look like?

- What does an auto insurance ID card look like?

- Is a digital insurance card valid as proof of insurance?

- How do I show proof of insurance if I don't have my card?

- What's the difference between a declarations page and an insurance card?

- What does full coverage car insurance look like on paper?

- Is My Policy Number on My Proof of Insurance Card?

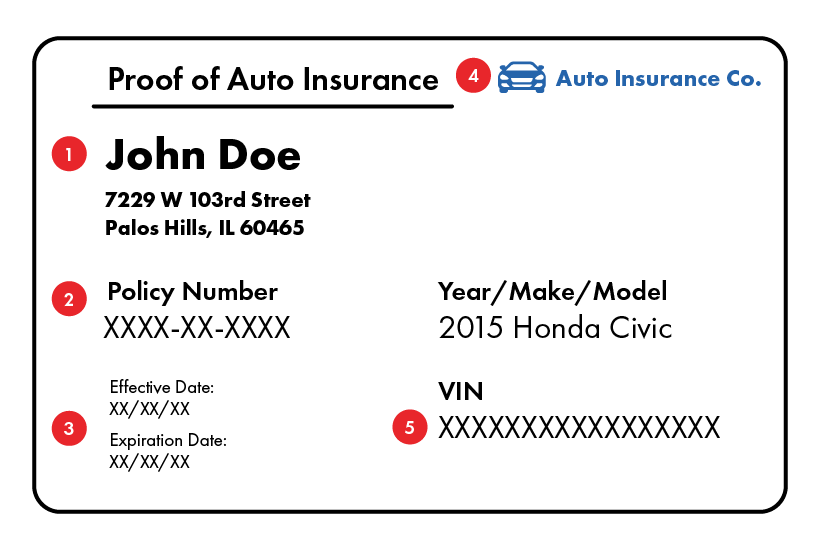

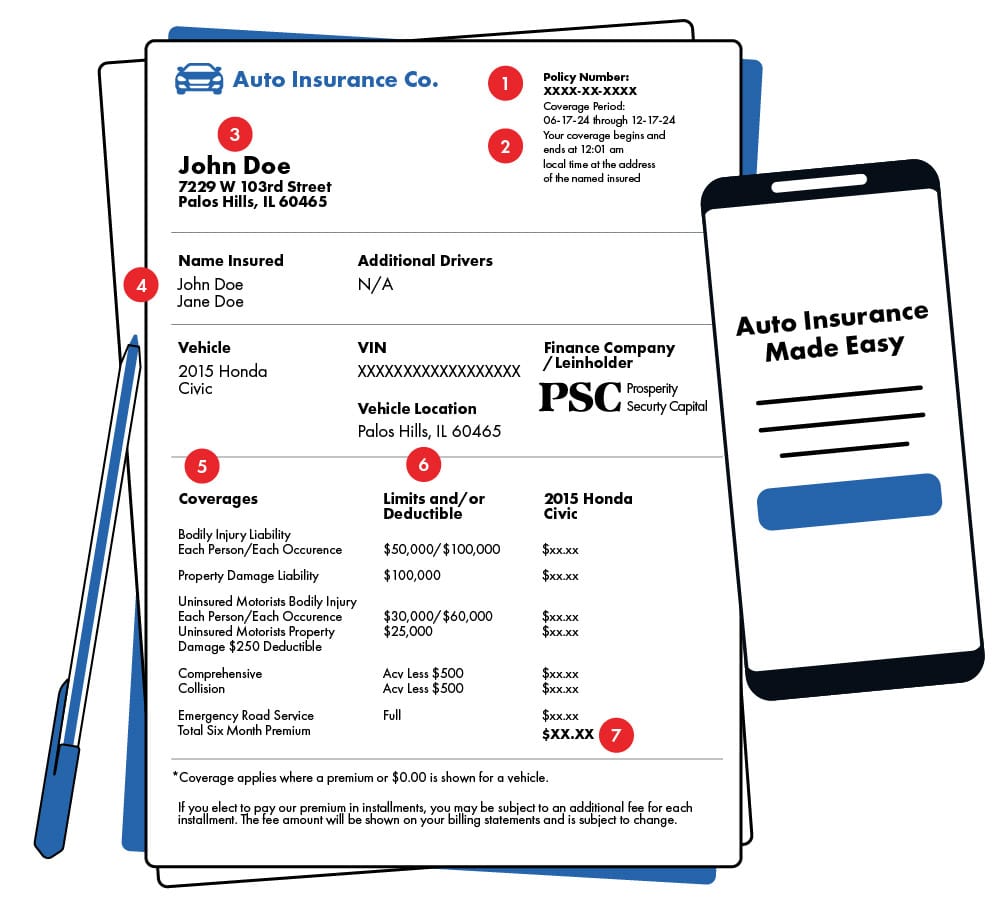

A car insurance policy looks like a multi-page document plus a wallet-sized ID card. The full policy runs 20 to 50 pages and contains ten standard sections. These sections are declarations, definitions, insuring agreements, conditions, coverages, limits, deductibles, exclusions, endorsements, and signatures. The proof-of-insurance card is the one-page summary you carry in your vehicle, showing your name, policy number, coverage dates, vehicle VIN, and your insurer's claims phone number.

This guide shows what each piece looks like in practice, using examples from major carriers including Progressive, GEICO, State Farm, Allstate, and Dairyland. It covers what's on a 2026 insurance card, what every section of a declarations page means, and how digital ID cards have replaced paper in 49 states.

What a Car Insurance Card Looks Like

The insurance ID card is the document drivers actually see day-to-day. It's printed on cardstock or displayed in a mobile app, roughly 3.5 by 2 inches when physical, and contains nine standard fields:

Insurance company name and logo, for example, "Progressive Casualty Insurance Company" or "State Farm Mutual Automobile Insurance Company."

Policy number, typically 8 to 13 digits or alphanumeric. Progressive uses 9 digits; State Farm uses 11; GEICO uses 10.

Named insured, the policyholder's full legal name as it appears on the application.

Effective and expiration dates, the six-month or twelve-month term the card is valid.

Vehicle year, make, model, and VIN, the 17-character Vehicle Identification Number.

Agent or company contact information, claims phone number, agent name, and local office address.

NAIC number, the five-digit National Association of Insurance Commissioners code that identifies the insurer to state DMVs.

Coverage codes, abbreviations like "BI" (bodily injury), "PD" (property damage), and "UM" (uninsured motorist), often with limits like 25/50/25.

State-specific notices, language required by your state insurance department, such as the Illinois Vehicle Code §3-707 reminder or California's mandatory disclosure.

Sample Card by Major Carrier

Insurance cards from different carriers share the same required fields but format them differently:

Progressive places the policy number at the top right, with vehicle and coverage details listed in two columns.

GEICO uses a horizontal layout with the gecko mascot in the corner and a 24/7 claims line (1-800-841-3000) prominently displayed.

State Farm issues red-and-white cards with the policy number formatted as XXX XXXX-FXX-XX.

Allstate includes a QR code on newer cards that links to the digital policy.

Dairyland and Bristol West (common SR-22 carriers) include an SR-22 indicator line when applicable.

Digital vs. Physical Cards

As of 2026, all states except New Mexico accept digital insurance cards displayed on a smartphone as legal proof of coverage during a traffic stop. The exception applies because New Mexico statute §66-5-205 still requires a physical card in some enforcement contexts. Most insurers, including Insurance Navy partner carriers, issue both a printable PDF and a wallet card via their mobile app within minutes of policy purchase.

What Your Car Insurance Policy Looks Like

Beyond the insurance card, your policy is broken down into sections. Knowing these sections will help you know what you're paying for and what you're covered for.

1. Declarations Page

The first page of your policy is the declarations page. It's a high-level summary of the insurance agreement. It lists:

Official headers and insignia of your insurance company.

Your name, address, and other identifying details.

Your car insurance policy number and policy effective/expiration dates.

Listed drivers and vehicles.

Types of coverage and corresponding limits.

Your annual or semi-annual premium.

Deductible amounts.

Any riders or endorsements added to your policy.

2. Agreements

The insurance company will provide the coverages listed in the policy in return for your premium. If you fail to pay, they can cancel the coverage per the insurance agreement.

3. Definitions

Key terms like "family members" or "insured drivers." For example, a policy might define family members as anyone related to you by blood, marriage, or guardianship who also lives in your household.

4. Insuring Agreement

This section states the types of coverage you have and when the insurance company will pay out. It also lists scenarios where coverages won't apply, like using your vehicle for business purposes without the correct coverages.

5. Conditions

Here, the insurer outlines what you must do if you have an accident and want to file a claim. Common conditions include:

A set time frame (e.g., one year) to file covered claims after an accident.

Requirements for reporting accidents to the police.

Procedures for canceling your policy or how the insurance company can cancel it.

6. Types of Coverage

Typical coverage types include:

Liability Coverage (Bodily Injury and Property Damage): This coverage, which is required in most states, covers injuries or damage you cause to others.

Collision Coverage: This covers the cost of repairing or replacing your car after an at-fault accident.

Comprehensive Coverage: Covers non-collision-related damage to your vehicle (e.g., theft, vandalism, natural disasters).

Personal Injury Protection (PIP): It helps pay for your medical expenses regardless of who is at fault.

Medical Payments Coverage: Similar to PIP, pays for Medical Bills as a result of an accident.

Uninsured/Underinsured Motorist Coverage: Uninsured Motorist coverage protects you if a driver hits you without sufficient insurance.

When collision and comprehensive coverage are included, the auto policy is often called full coverage.

7. Coverage Payment Limits

Each insurance coverage has a maximum amount the company will pay. These single limits are often shown as 25/50/20 which means:

$25,000 bodily injury liability coverage per person.

$50,000 bodily injury liability coverage per accident.

$20,000 property damage liability per accident.

8. Deductibles

The deductible is the amount you pay before the company pays the rest. Higher deductibles mean lower auto insurance premiums and vice versa.

9. Exclusions

This section clarifies what scenarios or damages the auto policy does not cover (e.g., intentional damage, impaired driving, or inevitable natural catastrophes).

10. Endorsements and Riders

Endorsements modify your policy to add or adjust insurance coverage. Some examples include:

Family Protection (extra coverage if an uninsured driver hits a family member)

Waiver of Depreciation (may cover a percentage of a vehicle's depreciation)

Loss of Use (covers the cost of a rental car while your vehicle undergoes repairs)

Why You Need to Carry Your Car Insurance Card

While having an active auto insurance policy is crucial, proof of that policy, in the form of an insurance card, can be equally important.

Think of it like a health insurance card: you must show it whenever you visit a doctor's office to validate your coverage. The same logic applies to auto insurance; you'll need proof of insurance to verify that you are operating your vehicle legally.

Situations Where You'll Need to Show Your Insurance Card

After a Car Accident: If you're involved in a collision, exchanging insurance information with the other driver is standard procedure. You'll need to provide your insurance card and policy number and, in return, obtain the other driver's information so you can file a claim with their insurance provider if they are at fault. If law enforcement is present, they may also ask for your insurance card to be included in the official accident report.

When Pulled Over By Police: In nearly every state, you must show proof of insurance when a law enforcement officer asks. Your insurance card, license, and vehicle registration confirm that you drive legally and meet mandatory insurance requirements. In most states, liability auto insurance is required before operating a vehicle.

When Contacting Your Insurance Company: Having your auto insurance policy number on hand is a must whenever you contact your insurance provider, to adjust your policy, make a payment, or ask a question. This number uniquely identifies your account, much like a bank account number, and simplifies any changes or inquiries.

What Else is on Your Insurance Card?

In addition to your policy number, insurance cards typically include:

Policyholder's Name and Address: Confirming the card belongs to you or another listed driver.

Insurance Company and Agent Details: Including the company's legal name, contact phone number, and sometimes your agent's name.

Vehicle Details: Year, make, model, and VIN (Vehicle Identification Number) of the insured car(s).

Coverage Information: Some cards list coverage types, deductibles, and effective dates.

Because many states now accept digital car insurance cards as valid proof of coverage, you can often store an electronic version on your smartphone.

However, printing and carrying a physical copy is still a good practice, especially in states like New Mexico, where law enforcement may not accept digital proof.

Losing Your Proof of Insurance Card

Misplacing your car insurance card happens more often than you might think. Fortunately, insurance companies are prepared to send replacement physical cards and can usually provide a digital or temporary version.

Even if you remember your policy number, always request a new physical or digital insurance card.

An outdated card might list incorrect information, and it's best to have official, updated proof of coverage handy, especially if you're pulled over or involved in an accident.

Embracing Digital Car Insurance Cards

With technological advancements, many drivers store their proof of insurance on a smartphone as an electronic or digital insurance card. While this is widely accepted in most states, you should check local laws.

In New Mexico, for instance, officers are not required to accept digital proof. Keeping both a digital and physical copy ensures you stay compliant everywhere you drive.

Ready to Shop for a New Policy?

If you're in the market for a new auto insurance policy or looking for more affordable coverage, Insurance Navy can help.

We offer various add-ons and coverage options at competitive rates. Connect with an agent at 888-949-6289 for a free quote, get started online, or visit one of our many storefront locations.

Key Takeaways

Always carry proof of insurance: You need your insurance card after an accident when pulled over and whenever you contact your insurer.

Know your policy number: This unique ID helps your insurer locate your account. You can have the same base number if you cover multiple vehicles.

Understand your policy's structure: From the declaration page to exclusions and endorsements, knowing each section ensures no surprises if you ever file a claim.

Embrace digital proof (when allowed): Digital cards are becoming the norm, but double-check local requirements to avoid issues with law enforcement.

Keep everything current: If you lose your card or any details change, get an updated version from your insurance company right away.

With a better grasp of what your car insurance card looks like, why it's essential, and how your policy functions, you're well-prepared to tackle the road, and any insurance questions that might come your way.