The average cost of car insurance is a national premium benchmark that shows how much drivers pay for coverage. Driving violations, vehicle type, location, and credit score raise the average cost of car insurance. U.S. car insurance premiums totaled $358.77 billion in 2024, according to S&P Global. That total makes private auto the largest property and casualty insurance line. Drivers need personalized quotes to compare rates across multiple providers. Insurance Navy helps drivers find affordable coverage at competitive rates. This guide explains the average cost of car insurance by state, rating factors, driving records, and discounts.

Table of contents

- How Much is Car Insurance?

- What Factors Affect Car Insurance Rates?

- How Much Does Car Insurance Cost by State?

- Average Car Insurance Costs by State in 2026

- Cheapest States for Full-Coverage Car Insurance

- Most Expensive States for Full-Coverage Car Insurance

- Car Insurance Rates Are Going Up

- How Do Driving Records Affect the Cost of Car Insurance?

- How Does Vehicle Type Affect Car Insurance Costs?

- How Does Age Impact Car Insurance Cost?

- How Does Gender Affect Car Insurance Costs?

- How Does Credit Score Affect Car Insurance Costs?

- How Can I Lower My Car Insurance Costs?

- Auto Insurance Discounts to Lower Car Insurance Rates

- Get a Free Car Insurance Quote Online Today!

On average, a full-coverage car insurance policy costs around $2,096 per year or $174 per month. Minimum coverage is $824 per year or $68 per month.

Prices vary depending on your coverage choice, driving history, age, gender, location, and vehicle type.

Car insurance prices vary by state and provider, so shop around to get the best policy.

Discounts, deductibles, claim frequency and history, credit score, coverage limits, and driving habits affect premiums.

How Much is Car Insurance?

Car insurance costs in the US vary by coverage type, driver profile, and location.

According to recent data, full coverage car insurance costs around $2,096 or $174 monthly.

In contrast, minimum liability only coverage costs $768 per year or $52 monthly.

Since 2023, full-coverage car insurance rates have risen 31% or $620 from the previous year.

Car insurance rates are highly personalized. Age, driving history, vehicle type, location, and coverage options impact your rates.

Even in the same area, two drivers with similar profiles will pay different premiums because of their unique rating factors.

National averages are a good guide, but you need personalized quotes to get competitive pricing and adequate coverage.

What Factors Affect Car Insurance Rates?

Several factors determine car insurance rates, each affecting how much you'll pay for coverage.

Auto insurers assess risk based on location, vehicle type, driving history, annual mileage, policy choices, and personal profile-including age, gender, marital status, credit and insurance history.

Since each insurance company weighs these factors differently, comparing multiple quotes can help you find the best coverage.

The Factors That Affect Your Car Insurance Premiums are listed below.

Age: Younger drivers, especially teens, pay more because they have a higher risk of accidents. Insurance rates decrease and stabilize as you get older.

Location: Urban areas with high theft, vandalism, and accident rates have higher premiums than rural areas. Each state also has different minimum coverage requirements, which impact your total cost.

Vehicle Type & Usage: Your vehicle's make, model, and safety features affect insurance rates. Luxury and sports cars cost more to insure because they're more expensive to repair and replace. You may pay more if you use your vehicle for business or ridesharing.

Driving History & Record: A clean driving record means lower premiums. Speeding tickets, at-fault accidents and other violations will result in insurance rate increases. However, many insurers remove surcharges for accidents or tickets after a certain period.

Coverage Selection & Deductibles: Higher coverage limits and lower deductibles mean higher premiums. State-minimum liability insurance is the cheapest option, but adding comprehensive and collision coverage increases the cost.

Annual Mileage: The more you drive, the more you risk having an accident, so you'll pay more. Some insurers offer usage-based discounts for low-mileage drivers.

Marital Status: Married drivers may see a slight decrease in their insurance rates since they file fewer claims.

Credit History: In many states, insurers use credit-based insurance scores to determine premiums. A better credit score means lower average rates.

Payment & Policy History: Paying in full, using electronic billing, and having continuous coverage without gaps can get you discounts.

Since each insurer weighs these factors differently, rates can change a lot between companies.

Compare personalized car insurance quotes and explore available discounts to save the most.

How Much Does Car Insurance Cost by State?

Car insurance prices vary by state for many reasons, including accident rates, claim frequency, labor and repair costs, vehicle theft rates, and road conditions. The coverage level a driver chooses also impacts the overall price.

To understand average costs, we'll examine the two most common coverage levels: full and minimum.

Drivers with leased or financed vehicles usually go with full coverage policies, which include comprehensive and collision coverage, with higher liability limits, such as 100/300/50.

Owners of older vehicles may choose a policy that only meets the state's minimum requirements. Minimum coverage only includes liability coverage, uninsured motorist coverage, and/or personal injury protection.

Since minimum coverage requirements vary by state, your car insurance price will be different in each state.

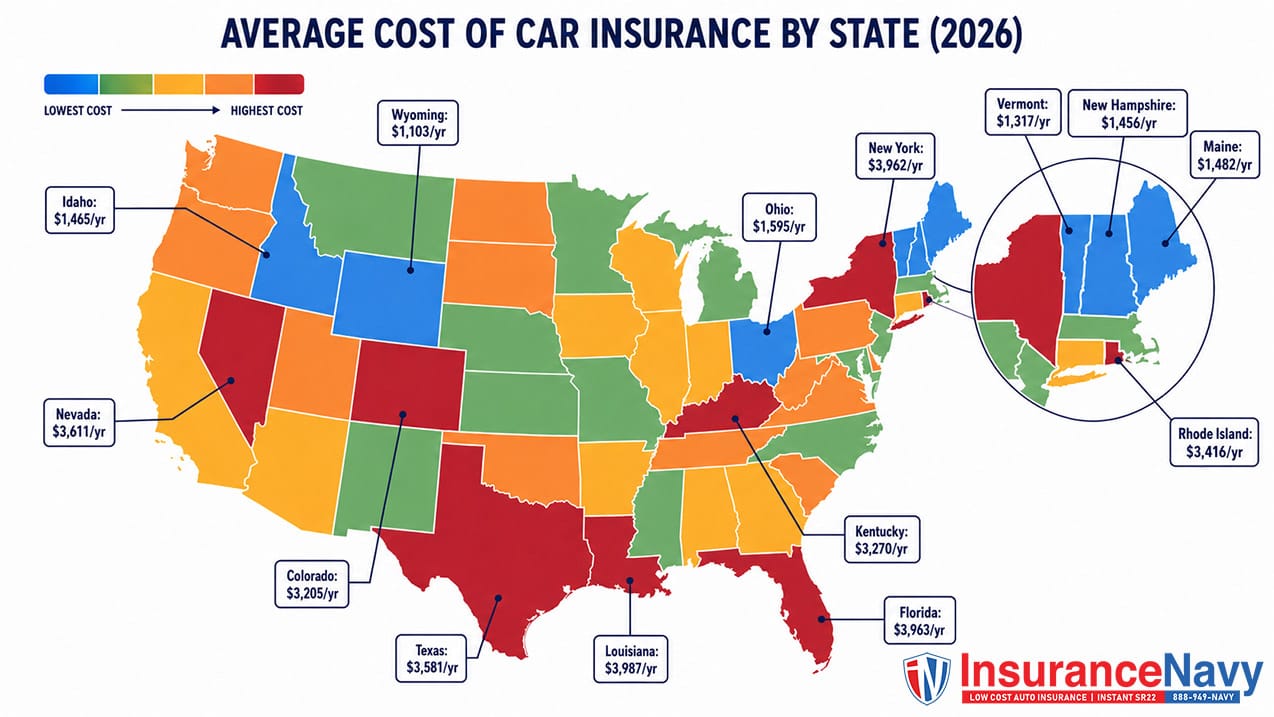

Average Car Insurance Costs by State in 2026

Rates vary by state, with some states having lower or higher prices based on economic and traffic factors.

States with lower cost of living, fewer claims, and less traffic congestion tend to be cheaper. States with dense populations, high repair costs, and higher medical costs are more expensive.

The national average cost for full-coverage car insurance in 2026 is $2,665 per year.

Cheapest States for Full-Coverage Car Insurance

Drivers in these states have some of the lowest annual car insurance rates.

The percentages are how much lower each state's average rate is than the $2,665 national average for auto insurance rates.

Wyoming: $1,103 per year - 59% below the national average

Vermont: $1,317 per year - 51% below the national average

New Hampshire: $1,456 per year - 46% below the national average

Idaho: $1,465 per year - 45% below the national average

Maine: $1,482 per year - 44% below the national average

Ohio: $1,595 per year - 40% below the national average

These states tend to have lower population densities, lower vehicle theft rates, and less traffic congestion.

When these factors don't pose higher risk like larger states, drivers will see lower car insurance rates.

Most Expensive States for Full-Coverage Car Insurance

These states have some of the highest annual car insurance rates. The national average for auto insurance premiums is $2,665.

Listed below, the numbers show how much higher each state's average rate is than the national average.

Louisiana: $3,987 per year - 49% above the national average

Florida: $3,963 per year - 48% above the national average

New York: $3,962 per year - 48% above the national average

Nevada: $3,611 per year - 35% above the national average

Texas: $3,581 per year - 34% above the national average

Rhode Island: $3,416 per year - 28% above the national average

Kentucky: $3,270 per year - 22% above the national average

Colorado: $3,205 per year - 20% above the national average

In urban areas, higher living costs and more accidents can contribute to higher insurance rates in these states as insurers account for the chances and severity of claims.

Car Insurance Rates Are Going Up

Car insurance rates have been rising for a few years, especially after the economic changes from the COVID-19 pandemic.

After a brief decline when fewer drivers were on the road, rates have skyrocketed since late 2021 with only minor fluctuations. This surge is mainly due to more severe accidents, more claims, and higher vehicle repair and replacement costs.

Knowing how car insurance costs vary by state can help drivers find cheaper rates.

Getting customized auto insurance quotes online and comparing different insurance companies is a good way to combat rising rates.

How Do Driving Records Affect the Cost of Car Insurance?

Your driving history matters a lot in terms of your car insurance rates.

A clean record means lower rates, about 6% below the national average car insurance rate. Traffic violations and accidents can cause rates to skyrocket.

For example, a single speeding ticket will raise your insurance premiums by about 21%, and an at-fault accident will increase your full-coverage from around $213 to $310 per month if it's your first offense.

Some insurance carriers offer accident forgiveness as an add-on, preventing a rate increase for a first-time accident.

The biggest rate increase is from a DUI conviction. A DUI can increase your rates by almost 79% above the national average.

Depending on state laws, a DUI can stay on your record for 10+ years. Insurance costs after a DUI depend on the state. Full coverage for drivers with a DUI can range from $2,174 - $7,461 depending on state.

Beyond higher insurance costs, multiple violations or serious infractions can make you a high-risk driver and limit your coverage options. Many states use a points-based system to track traffic violations.

A minor infraction like failing to yield is 3 points, and a more serious offense like hit-and-run is 6 points. You'll get a license suspension if you accumulate too many points within a certain period.

Even states that don't have a formal points system still monitor your driving history, which insurers consider when setting rates.

To keep your rates affordable, practice safe driving, follow speed limits, obey traffic laws, and never drive under the influence.

A clean record gets you lower rates and keeps you eligible for competitive coverage options.

How Does Vehicle Type Affect Car Insurance Costs?

The type of vehicle you drive plays a major part in your car insurance premiums price. Major factors such as repair costs, part availability, accident statistics, and safety features determine to the cost of insurance for different types of vehicles.

Insurance costs differ widely depending on the vehicle's size, value, and safety profile.

Mid-size sedans and SUVs have the lowest insurance rates since they balance safety, affordability, and repair costs.

Some cars are more expensive to insure because of higher repair costs, increased accident risk, or higher theft rates.

Vehicle Types That Are More Expensive to Insure are listed below.

Luxury and Sports Cars: High end vehicles are more expensive to insure because of higher replacement costs, specialized repairs, and high cost of labor. Sports cars are riskier because of their powerful engines and high speed, which increases the chance of accidents.

Large SUVs, Vans, and Trucks: Bigger vehicles provide more protection to their passengers. On the negative side, they are capable of causing more damage to other vehicles and pedestrians.

Economy Cars Prone to Theft: Some cheaper cars with fewer security features, are more likely to be stolen. They need comprehensive coverage to replace the car. Some low-cost models like Hyudia and Kias are frequent theft targets due to bad security technology.

Electric and Hybrid Vehicles: EVs and hybrids are still more expensive to insure than gas powered cars. Their high tech components, expensive battery systems, and specialized repairs can increase comprehensive coverage rates.

Vehicles with Low Safety Ratings: A car with poor crash test ratings or fewer safety features may have higher insurance costs since they are more prone to accidents and more damage in case of an accident.

Choose a vehicle with high safety ratings, advanced security features, and average repair costs. This will help keep your insurance premiums affordable.

How Does Age Impact Car Insurance Cost?

Age is a significant factor in car insurance rates. Age is linked to driving experience, accident risk, and how often claims are filed.

Insurers use statistics on age groups to assess risk of claims. This leading to different price variations across age groups.

Teenagers and young adults in their early 20s pay the highest car insurance prices due to their lack of experience and higher accident rates.

Research shows that teen drivers are more likely to be involved in speeding accidents, nighttime accidents, and driver error accidents. So, insurers charge much higher premiums to offset the risk.

Once drivers reach their mid-20s, insurance rates decrease as long as they have a clean driving record. Rates continue dropping until age 60 as accident risk decreases with experienced drivers.

However, insurance rates started to rise again for drivers in their 70s. Age-related declines in reaction time, vision impairment, and potential health conditions increase the chances of an accident, leading to higher premiums for senior drivers.

Fatal crash rates are highest for drivers over 80, followed by teenagers and young adults 16-24.

No matter the age, safe driving, minimal violations, and finding discounts can help get lower insurance rates over time.

How Does Gender Affect Car Insurance Costs?

In most states, gender matters for car insurance, especially for younger drivers.

On average, men pay more than women because of riskier driving and higher accident rates. As drivers get older, the gap narrows a lot, and by age 30, the rates are almost the same.

Teenagers and young adults see the most significant difference in car insurance rates based on gender.

At 16, men pay about 14% more for full coverage than women. A 16-year-old male pays $5,866 annually.

A 16 year old female of the same age pays $387 less ($5,479 annually).

By 20, men pay 11% more than women; by 25, it's 5%; by 30, the difference is nothing; by 40, it's 1%; and for senior drivers, 60+, gender has no impact.

Not all states allow gender pricing. In California, Hawaii, Massachusetts, Michigan, North Carolina, and Pennsylvania, insurers can't use gender as a rating factor, so men and women pay the same rates for the same policy.

These laws prevent discrimination in insurance pricing and make premiums based on driving history and other risk factors, not gender.

Men usually pay more for car insurance, but there are exceptions where women pay slightly more. In Florida, women pay $194 more than men. In Oregon, women pay $125 more per year then men.

How Does Credit Score Affect Car Insurance Costs?

In most states, credit score has a major effect on pricing car insurance rates. Insurance companies use credit based insurance scores from drivers credit history. This helps determine how likely they are to file a claim.

This insurance based credit score is not the same as a traditional credit score. It is based on similar factors like payment history, outstanding balances, and credit limits.

Drivers with bad credit based insurance scores are more likely to file claims. This makes them higher risk customers. The insurance company compensates for this risk by charging higher insurance premiums.

Insurance costs fluctuate by credit tier. The average costs for an auto policy by credit tier are listed below.

Excellent credit pays around $126/month for full coverage.

Good credit pays around $140/month.

Fair credit pays around $153/month.

Poor credit pays significantly more at $186/month.

Drivers with poor credit pay nearly 76% more for full coverage than those with good credit. This is because insurers view poor credit as a higher financial risk.

Statistically, drivers with low credit-based insurance scores are more likely to file claims, and insurance providers must charge higher premiums to drivers with poor credit scores.

A few states have banned the use of credit history when calculating car insurance rates. In California, Hawaii, Massachusetts, and Michigan, insurers are not allowed to use credit when setting premiums.

Other states, like Maryland, Oregon, and Utah, allow credit-based pricing but prohibit insurers from using credit history to deny, cancel, or refuse policy renewal.

Credit-based insurance scores are among the many factors that go into rates, so drive safely, take advantage of policy discounts, and shop around for the best rates to get affordable car insurance coverage.

How Can I Lower My Car Insurance Costs?

Car insurance rates are rising, but there are ways to lower your premiums without sacrificing coverage.

By taking proactive steps such as comparing quotes, adjusting your policy, and driving safely, you can save hundreds a year on car insurance.

Compare Insurance Quotes - Insurance rates vary between companies, so get quotes from multiple providers before you buy or renew your policy to find the best deal.

Take Advantage of Discounts - Ask your insurer about discounts for bundling home and auto insurance, installing safety features on your vehicle, attending a defensive driving course, or being claims-free.

Adjust Your Coverage Amount and Deductible -Increasing your comprehensive and collision insurance deductibles will lower your monthly premium, but be prepared for higher out-of-pocket costs if you have to file a claim. Consider dropping optional coverages on older vehicles.

Improve Your Credit Score - In most states, insurers use credit-based insurance scores to determine rates. Paying bills on time, reducing outstanding balances, and having a healthy credit mix can help you qualify for lower premiums.

Reduce Your Mileage - If you drive fewer miles than the average driver, you may be eligible for low-mileage discounts. To reduce your mileage, carpool, use public transportation, or work from home.

Keep a Clean Driving Record - Avoid speeding tickets, at-fault accidents, and other violations, as these can increase your rates. Safe drivers qualify for extra discounts.

Consider Telematics and Usage-Based Insurance - Some insurers offer telematic programs that track your driving habits through a mobile app or device in your car. If you drive safely and infrequently, these programs can lower your premium.

Using these strategies, you can cut your car insurance premiums while keeping the necessary coverage.

Auto Insurance Discounts to Lower Car Insurance Rates

Car insurance companies offer discounts to help you lower your insurance premiums.

Car insurance discounts are based on driving history, policy bundling, vehicle type, and payment methods. Take advantage of these, and you'll save big on auto insurance.

Claims-Free Discount - If you have no claims on your record for the last 3 to 5 years, you may qualify for lower premiums with a safe-driving or claims-free discount.

Safe Driver Discount – Keep a clean driving record with no accidents, violations, or significant claims for several years, and you'll get extra savings.

Driver Training Discount – Young drivers who complete an approved driver education course may qualify for a discount.

Good Student Discount -You'll get lower rates if you have high school or college students who maintain a "B" average (3.0 GPA or higher) on your policy.

Student Away at School Discount – If a student on your policy attends school at least 100 miles away and doesn't regularly drive, you may be eligible for reduced premiums.

Multi-Policy Discount – Bundle auto insurance with homeowners, renters, motorcycles, umbrellas, or other policies, and you'll save big.

Multicar Discount – Insure two or more vehicles under the same policy, and you'll get lower rates.

Homeowner Discount - Even if your home or condo is insured elsewhere, owning a home may qualify you for a discount on car insurance.

New Car Discount - You may qualify for lower rates if you buy a new car or own a vehicle less than three years old.

Hybrid/Electric Car Discount - Eco–friendly drivers who own or lease a hybrid or electric vehicle may qualify for discounts.

Pay-in-Full Discount – Pay your entire premium upfront (annually or semi-annually) instead of monthly, and you'll get lower costs.* Auto Pay Discount – Set up EFT or payroll deduction, and you'll get additional service fee savings.

Paperless Discount – Get a small discount on your bills and policy documents.

Early Quote Discount - New customers who get a car insurance quote before their current policy expires will receive discounted rates.

Loyalty and Continuous Insurance Discount – Drivers with continuous car insurance coverage with no gaps are usually eligible for lower rates.

Stacking discounts can help you save big and lower your car insurance costs. Check with insurers often and stay informed about discounts to get the best rate possible.

Get a Free Car Insurance Quote Online Today!

Looking for the cheapest car insurance that fits your budget? Insurance Navy automatically compares rates for you to find you the cheapest price with the best coverage.

Looking for cheap car insurance without sacrificing quality? Let Insurance Navy’s knowledgeable insurance agents help you find the best policy.

They will walk you through coverage options, discounts, and more so you buy the best insurance possible!

Call Insurance Navy today or get a free quote online to start saving on your car insurance!